No matter what part of your life you are currently in, eventually you will want to retire, even if it seems a long way off. These tips on retirement saving will do the most for you when you do them in order, so we’ll start with number one, and you've already half completed it.

Tip #1: Make a Plan

Think about retirement savings and make a plan. By far, the most frequent cause of poor financial retirement outcome is failure to even contemplate it. Without a plan there is no action, not even partial action, no triggers to step up efforts, and no measure to gauge progress.

To make your plan, there are a number of retirement calculators available online to help you decide approximately how much money you’ll want to have and when. Armed with this target, you can see if you are able to save enough or whether you need to reduce your current spending to make up the difference. The calculators will help you factor in adjustments to the saving strategy such as interest rates and employer matching. Once you have this ballpark target, you can start to apply the next tips.

Tip #2: Save Early

Don’t wait until you have the more comfortable job you’re seeking at your next promotion. Don’t wait until the kids are out of daycare. Don’t wait until the car is paid off. All of these other demands on your budget are essentially ever-present. As soon as you can cross off daycare fees, you’ll start paying sport team fees and other school fees, and the end-point of those expenses will never really arrive. Instead, start saving now, despite those other budget items and make time do the heavy lifting. Each additional ten years you save gives you a chance to let time double your money if you are earning a 7% return.

Tip #3: Save Regularly and Before Counting the Money in Your Budget

Money that you set aside automatically and outside of your household budget is easier to part with and easier to sustain. If you find yourself making retirement savings after you have paid the electric and the shopping bills, you’ve created a competition for resources and the far-off retirement will always seem like a good payment to delay. It’s best to make your transfers to your retirement account as early in your compensation path as possible. A transfer directly through payroll into a retirement account is the best, or your bank can divert some of your funds as they receive a direct deposit. If you take a physical check, you can make your retirement deposit the first thing that you do at the bank window. Make it a bill that you pay to yourself as soon as you receive your pay.

Tip #4: Exploit Add-ons and Extenders

After your own savings, the largest contributor to your bottom line is employer matching. If your employer offers matching funds to your retirement savings account, you should maximize this benefit and let your employer build your retirement with you; it is a better and more secure return than any interest rate. Look also for ways to increase your pension benefit if you have one and take advantage of tax-deferral in IRA accounts to build your nest-egg faster than savings alone.

There are many other avenues to help improve your retirement outlook, including downsizing earlier, working a little later, deferring Social Security payments from the minimum of age 62 to the maximum of 70 as a start-date, and optimizing Medicare insurance strategies. But saving remains the area you can best control to provide the retirement you want to enjoy. These tips will help you make the most of that segment of your portfolio and provide the foundation to a secure and comfortable retirement.

Sam M. is a financial blogger who has recently begun his retirement savings and writes from his experience. He also writes about other topics that may be of interest including how to go about getting Medicare supplement insurance and how to find life insurance that’s affordable.

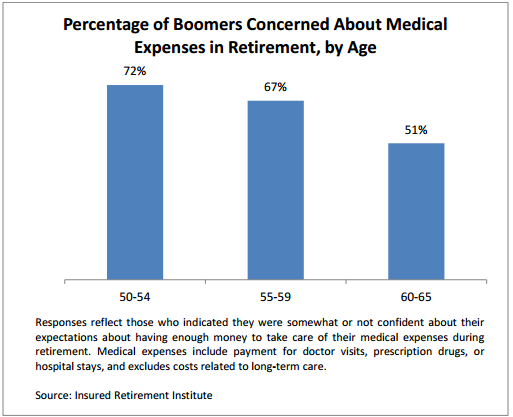

Retirement (Photo credit: 401K)Boomers are worried if they can afford health care costs in retirement. A report by the Insured Retirement Institute found two-thirds of boomers aren’t confident they have enough saved to cover the cost of health care after they retire. Also 72% of the younger boomers, between 50 and 54, say they are concerned about health care costs.

Retirement (Photo credit: 401K)Boomers are worried if they can afford health care costs in retirement. A report by the Insured Retirement Institute found two-thirds of boomers aren’t confident they have enough saved to cover the cost of health care after they retire. Also 72% of the younger boomers, between 50 and 54, say they are concerned about health care costs.